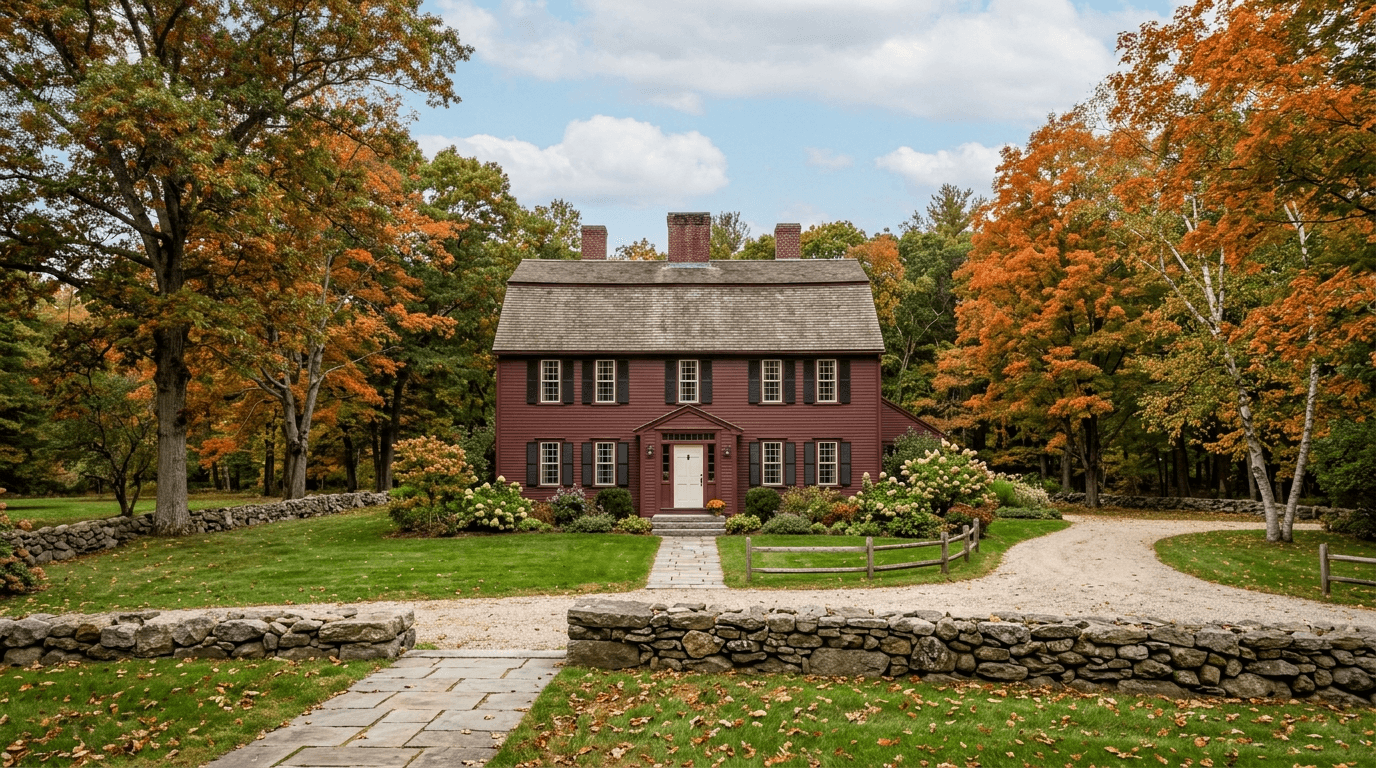

# March Buyers Capitalize on Concord's High-End Pricing Recalibration

Key Takeaways

•The Direct Answer: While Concord MA property taxes are undeniably high, they are a phenomenal investment because they fund elite School District Tiers and community amenities that permanently protect your home's value.

•The Current Opportunity: A mid-March 2026 rate shock has temporarily thinned out competition, giving buyers rare buyer negotiating leverage to offset tax costs with lower entry prices.

•The Bottom Line: Don't wait for the traditional spring surge; buying now allows you to secure a premium lifestyle and long-term wealth preservation before the inventory bottleneck drives prices higher.

Is the Concord Tax Bill a Dealbreaker or a Hidden Advantage?

Most people think Concord's high property taxes automatically make it a bad investment. But March 2026 is telling a different story. With high-end pricing recalibrating and buyers pushing for value, your tax bill can become the "known cost" that buys you premium school zones and rare negotiating leverage.

If you're asking, "Concord has high property taxes—is it still a good investment?"—you're thinking like a responsible buyer.

You've probably fallen for the homes, the schools, the trails, the village centers. Then you see the tax line item and start wondering if you're walking into a financial mistake.

Here's a better way to think about it: in a town like Concord, high taxes aren't just a cost—they're part of the value proposition that keeps demand, and prices, durable.

What Does Your Tax Bill Actually Buy You Every Day?

Concord's tax premium shows up in your daily life, not just your escrow payment.

When you buy into Concord MA real estate, you're buying an experience: strong public safety, well-maintained roads and facilities, protected open space, and a community that actively preserves what makes it worth living in.

That matters because desirability is what protects resale value. The more consistently a town delivers on quality of life, the more "sticky" buyer demand becomes—especially at higher price points.

And to understand why that stickiness holds in Concord, you have to look at who chooses to live here.

Concord, MA Demographic Snapshot

Quick context on Concord’s population, age, income, and density. Uses a snapshot to accommodate mixed units and text.

Census (as provided)

Total Population18,237

Median Age46 years

Average individual Income$96,679

Population DensityHigh

The data points to a high-income, highly educated demographic with clear expectations—and they don't settle.

What does that mean for you? There's a deep bench of future buyers who will pay a premium for the same fundamentals you're buying today: school quality, community standards, and a town that has deliberately stayed itself.

Because Concord is well-funded, the relationship between Assessed Value vs Market Value also tends to stay stable—which reduces the odds of unpleasant "surprise math" when you eventually sell.

How Did the March 2026 Rate Shock Create a Window for Buyers?

Here's what's happening right now in mid-March 2026: mortgage rates jumped—fast.

Rates surged to a 7-month high of 6.41% on March 13, 2026.

That spike didn't just change affordability. It changed buyer psychology. Some buyers paused, and that pause creates something Concord almost never offers:

breathing room.

February's market backdrop shows just how tight things were before this shift.

Concord, MA Market Snapshot (February 2026)

Headline market pulse for Concord: current single-family inventory and median price (mixed units shown together).

February 2026

Single-family homes on the market13

Median price$2.6M

With a median price of $2.6M and only 13 single-family homes on the market last month, sellers held all the cards.

The rate shock changes that math. When fewer serious bidders show up, you're in a much stronger position to negotiate:

•a price reduction

•a seller credit (especially useful for offsetting closing costs or buying down your rate)

•cleaner inspection and financing terms, without the pressure to waive protections you actually need

That's real, tangible leverage—and it can meaningfully blunt the sting of high property taxes by improving your entry price or reshaping your monthly payment structure.

Data Table

| Market Metric | Typical Spring Frenzy | March 2026 Reality | Buyer Impact |

|---|---|---|---|

| Competition | 5-10 offers per home | 1-2 serious offers | High negotiating leverage |

| Pricing | Bidding wars over asking | Sellers accepting list or slightly below | Better entry price |

| Contingencies | Waived inspections | Standard protections accepted | Lower risk for buyers |

Should You Wait for the Spring Market to Buy in Concord?

Waiting is tempting—either for rates to settle or for the "normal" spring inventory surge to materialize.

The practical risk? If rates ease even slightly, paused buyers tend to re-enter fast. In Concord, that can flip you right back into multiple-offer territory almost overnight.

Waiting can cost you twice: you lose today's negotiating leverage, and you still inherit the same tax structure later—just at a higher purchase price.

And that spring inventory surge? The data isn't backing it up.

Data Table

| Concord Inventory Snapshot | Current Data | Market Reality |

|---|---|---|

| Active Listings | 56 homes | Historically low for spring |

| New Listings (Recent) | 11 homes | Not enough to meet pent-up demand |

| Days on Market (Hot Homes) | 10-14 days | Fast turnover for prime properties |

With only 11 new listings recently and 56 active listings total, this isn't a surge—it's a bottleneck.

For your timeline, that means one thing: if a home checks your boxes on schools, commute, and lifestyle right now, waiting raises the odds you'll have fewer choices later and pay more to get them.

Are Concord's Amenities Worth the Premium Price Tag?

Honestly? You don't buy Concord because it's the cheapest option. Nobody does.

You buy Concord because the town converts money into durable, visible value—and the single biggest driver of that value is the Concord-Carlisle school system.

School District Tiers are a major engine of suburban pricing power. When a district is consistently high-performing, families plan around it, relocate for it, and compete for it—year after year, regardless of what the broader market is doing.

Financially, strong schools tend to stabilize demand in softer markets, compress time-to-sell for well-located homes, and support premium pricing when you're ready to exit.

But it's not only schools. Concord is a destination—and that's a quiet signal of sustained desirability.

Hotel Occupancy (Occ) — 2022 vs 2021 (YTD December)

Compares occupancy rates across regions for 2022 vs 2021 (all values are percentages).

Occ (2022)

Occ (2021)

Average Daily Rate (ADR) — 2022 vs 2021 (YTD December)

Compares ADR across regions for 2022 vs 2021 using the numeric values as presented in the source table.

ADR (2022)

ADR (2021)

Notice how hotel Average Daily Rate (ADR) and occupancy remain strong. That's a proxy for a place people actively choose—because of history, outdoor access, and proximity to Boston. Your property taxes help maintain the environment people travel to experience. You get to live in it every day.

That kind of town "brand strength" doesn't fade quietly. It supports long-term resale demand in ways that are hard to replicate elsewhere.

Is This Property a Good Investment for Your Family?

Yes—Concord can be a strong investment even with high property taxes, because those taxes fund the very qualities that protect long-term value: elite schools, public safety, preservation, and community consistency that doesn't erode over time.

Right now, in mid-March 2026, the rate-driven slowdown is handing buyers something genuinely rare in this market: negotiating leverage. That leverage translates into a better entry price, better terms, or both—two levers that can effectively offset the tax bill over the life of your ownership.

Want the numbers for your specific situation? Send me the address—or a few listings you're weighing—and I'll break down estimated taxes, likely negotiation room based on current competition, and what your monthly payment could look like with and without seller credits.